实盘配资

细楷配资 华泰宏观解读5月FOMC决议:联储平息加息疑虑,6月开始削减缩表

专题:美联储维持基准利率不变 将从6月开始放缓缩表步伐

转自:华泰证券宏观研究

核心观点

北京时间5月2日(周四)凌晨,联储5月FOMC决议将基准利率维持在5.25%-5.5%区间;缩表方面,如我们在5月FOMC预览中的预期,联储6月开始将月度缩表上限从950亿美元(600亿国债+350亿MBS)放缓至600亿美元(250亿国债+350亿MBS),超过MBS上限的本金收入将再投资到国债市场。在新闻发布会上,鲍威尔表示即使通胀不再下降,联储也会保持利率在目前水平继续观察,而再次加息可能性低(unlikely)。我们解读如下:

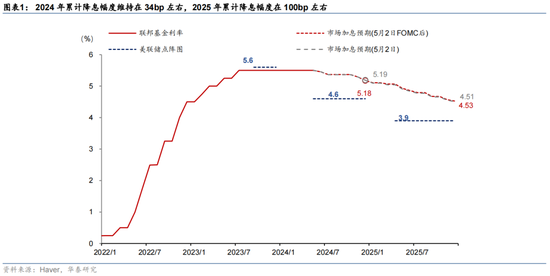

总体而言,联储5月决议基本符合市场预期,但鲍威尔在发布会上的表态偏鸽派。对市场而言,本次FOMC最重要的效果是“收窄了”联储可能政策路径的路径猜测,从此前包括加息在内、较为“发散”的路径假设回到“分歧仅在降息时点上”。鲍威尔表示对1季度通胀数据的反复不宜过分解读,同时,强调薪资通胀趋势性回落、及房租通胀将继续下行,仍预期今年通胀将回落。截至北京时间凌晨7:30,相较于会前,9月降息的概率微降至65%;2年期和10年期美债收益率分别回落4bp和2bp至4.96%和4.63%(图表1)。考虑到美国此后的大选议程我们认为,目前市场计入的降息路径可能是“7月开始降息两次”和“不降息”这两种分歧较大(binary)的可能性加权平均的结果,联储倾向仍然偏鸽,最终哪种路径更有可能发生将取决于4-5月的通胀走势。

增长方面,联储对增长前景仍然较为积极,鲍威尔强调存在软着陆的可能性。鲍威尔表示,尽管GDP数据不及预期,但对潜在需求指示意义更强的私人国内购买需求(GDP剔除存货、政府购买和净出口)维持2023年下半年以来的较强增长。尽管高利率对住房和设备投资有一定制约,但消费维持韧性,供给持续改善也对增长形成支撑。劳动力市场方面,就业仍然偏紧但劳工再平衡仍在持续:25-54岁劳动参与率持续改善以及移民持续流入推动劳工供给明显增加,而名义工资增速放缓、岗位与就业缺口收窄显示“劳工荒”或边际缓解,但劳工需求仍超过供给。

通胀方面,鲍威尔承认近期通胀进展陷入停滞,但仍然预计未来通胀会回落。FOMC声明中,联储新增了“最近几个月通胀缺乏进一步进展(lack of further progress)”的表述。鲍威尔表示,一季度通胀高于预期,暗示去年年底的金融条件宽松可能是背后的原因。鲍威尔仍然预测今年通胀可能会降温:例如工资增速持续放缓,住房通胀分项将滞后回落。通胀预期方面,鲍威尔表示,近期短期通胀预期有所加速,但中长期通胀预期仍然相对稳定。

往前看,货币政策可以总结为,延迟降息的门槛不高,而加息的门槛很高。前者符合市场预期;后者缓解市场部分担忧。鲍威尔表示,年初以来的数据通胀超预期,导致联储对通胀回到目标的信心有所下降,联储可能需要比之前预期更长的时间才能有足够的信心降息,联储可能推迟降息。此外,鲍威尔认为不太可能再次加息:当前的货币政策仍然具有限制性,经济持续强劲,加上通胀进展持续停滞,只会导致美联储推迟降息;重新考虑加息需要有令人信服的证据来证明当前利率没有足够限制性,无法将通胀持续降至2%。联储降息前景取决于就业市场和通胀数据,例如劳动力市场出现实质性的、意想不到的疲软以及通胀恢复去年的下降趋势。

综上,本次FOMC的信号中性略偏鸽,对市场而言,本次发布会最重要的效果是“收窄”了市场对此后联储路径的猜测,基本排除了加息的可能性——虽然最后加权平均的降息预期改变不大,但这次会议减少了市场预期的多样性,边际降低了风险溢价。正如我们会前预测(《5月FOMC预览:降息仍需观察,但或宣布Taper》,2024/4/28),近期联储推迟降息预期是对一季度偏高的增长和通胀数据合理和必然的反应,考虑到联储认为目前政策已处于限制性区间,如果后续数据允许,联储仍有较强的意愿在今年开启降息。鲍威尔这次的讲话显示,联储降息的两种可能情形是就业市场出现实质性、超预期放缓以及通胀恢复下行趋势。近期公布的就业数据显示新增就业维持较强水平,但这可能和移民大量涌入的结构性变化有关,联储对此的敏感度可能下降(参见《美国:人口流入的宏观影响不容小觑》,2024/4/21)。同时,联储更为重视的薪资走势显示,就业市场整体仍在持续降温。我们将密切关注明天(5月3日)发布的非农数据是否进一步验证这一趋势。考虑到美国此后的大选议程我们认为,目前市场计入的降息路径可能是“7月开始降息两次”和“不降息”这两种分歧较大(binary)的可能性加权平均的结果,联储倾向仍然偏鸽,最终哪种路径更有可能发生将取决于4-5月的通胀走势。若4-5月通胀能够持续位于0.3%以下(即年化3%以下),7月降息仍然存在一定概率,但如果持续高于0.3%(年化3-4%),7月降息可能性较小。

风险提示:通胀粘性导致联储鹰派超预期,高利率导致美国金融风险暴露。

附录:5月和3月FOMC声明的对比

Recent indicators suggest that economic activity has been expandingcontinued to expand at a solid pace. Job gains have remained strong, and the unemployment rate has remained low. Inflation has eased over the past year but remains elevated. In recent months, there has been a lack of further progress toward the Committee‘s 2 percent inflation objective.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are moving intohave moved toward better balance over the past year. The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. In considering any adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage backed securities, as described in its previously announced plans.Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion. The Committee will maintain the monthly redemption cap on agency debt and agency mortgage backed securities at $35 billion and will reinvest any principal payments in excess of this cap into Treasury securities. The Committee is strongly committed to returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee‘s goals. The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Philip N. Jefferson; Adriana D. Kugler; Loretta J. Mester; and Christopher J. Waller.

股市回暖,抄底炒股先开户!智能定投、条件单、个股雷达……送给你>>

海量资讯、精准解读,尽在新浪财经APP

海量资讯、精准解读,尽在新浪财经APP

责任编辑:刘明亮 细楷配资